Contribution Margin vs. Gross Profit: Why Variable Costing Wins for Management Reporting

Contribution Margin vs. Gross Profit: Why Variable Costing Wins for Management Reporting

Meta description: Discover why contribution margin under variable costing provides better insights for internal management than gross profit under absorption costing.

Financial accounting serves investors and regulators. That’s why external reporting (GAAP/IFRS) requires absorption costing, which culminates in the familiar Gross Profit line. Essential for the financial statements—yes. But for internal decisions, Gross Profit can mislead.

Managers need a line of sight into cost behavior, volume sensitivity, and real economics of product and channel choices. This is where variable costing—and its core metric, contribution margin—outperforms gross profit as a management lens.

Why Gross Profit Can Mislead

- Fixed overhead is absorbed into inventory. When production exceeds sales, a portion of fixed costs is capitalized, making profits look healthier even without extra sales.

- Volume bias. Managers can inflate reported profit by producing more, tying up cash and space in inventory.

- Behavior is hidden. Gross Profit doesn’t separate variable and fixed costs, limiting CVP and break-even insights.

Key point: Gross profit is excellent for external reporting, but it can distort managerial decisions when inventory moves independently of demand.

Variable Costing: The Clearer Lens

Under variable costing, only variable manufacturing costs are assigned to units; fixed manufacturing costs are expensed in the period. This yields the contribution margin:

Contribution Margin = Sales − Variable Costs

- Clarity of cost behavior (variable vs. fixed) for sensitivity and scenario analysis.

- Break-even ready: Directly supports cost–volume–profit analysis and operating leverage.

- Decision relevance: Clear view of pricing, product mix, and make/buy choices.

- No inventory distortion: Overproduction doesn’t artificially boost income.

Illustration (Simplified)

Assume a widget with price 100, variable cost 60, and monthly fixed manufacturing overhead 120,000. In Month 2 the factory overproduces relative to sales. Under absorption costing, some fixed overhead is parked in inventory—reported gross profit rises. Under variable costing, it doesn’t.

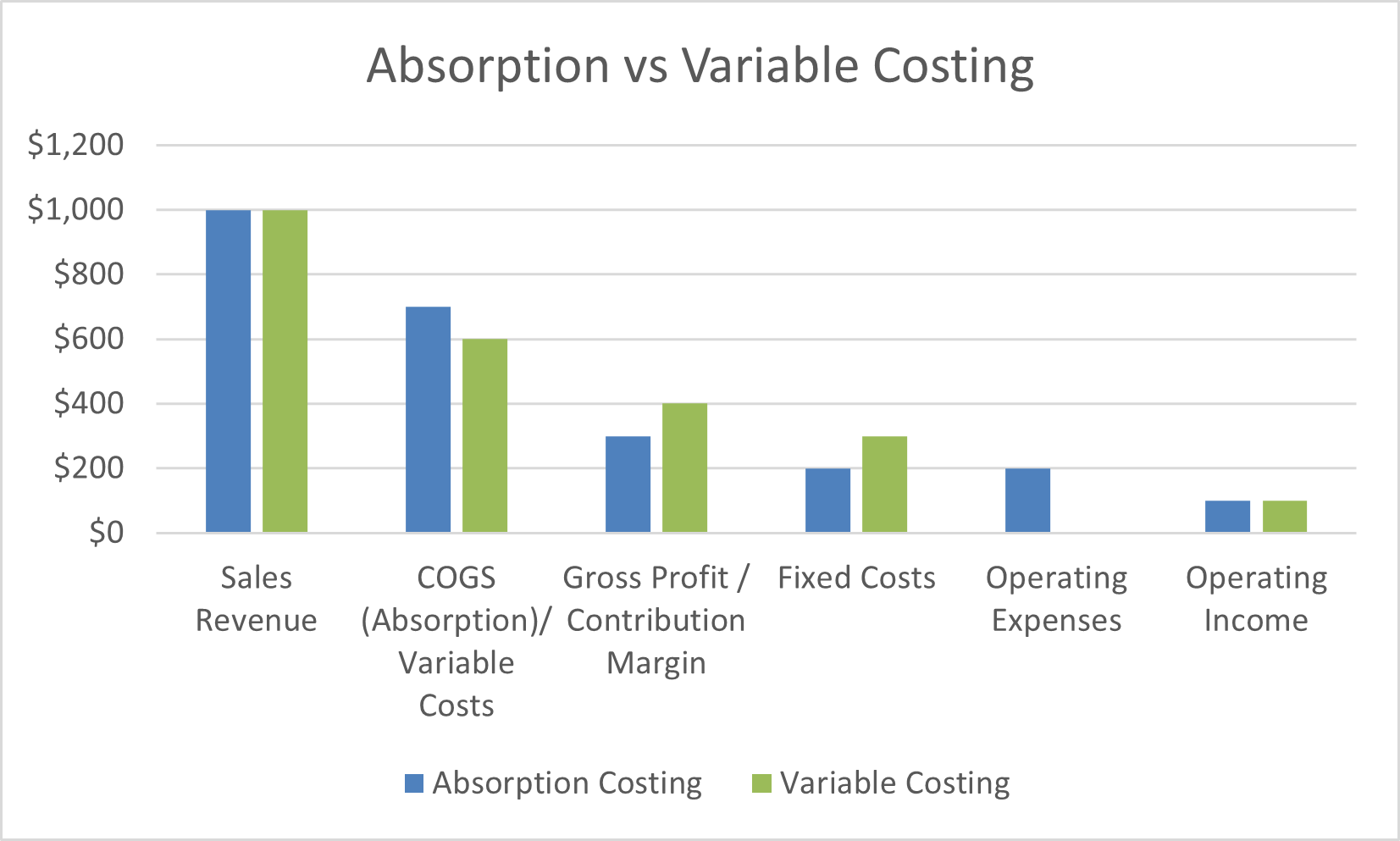

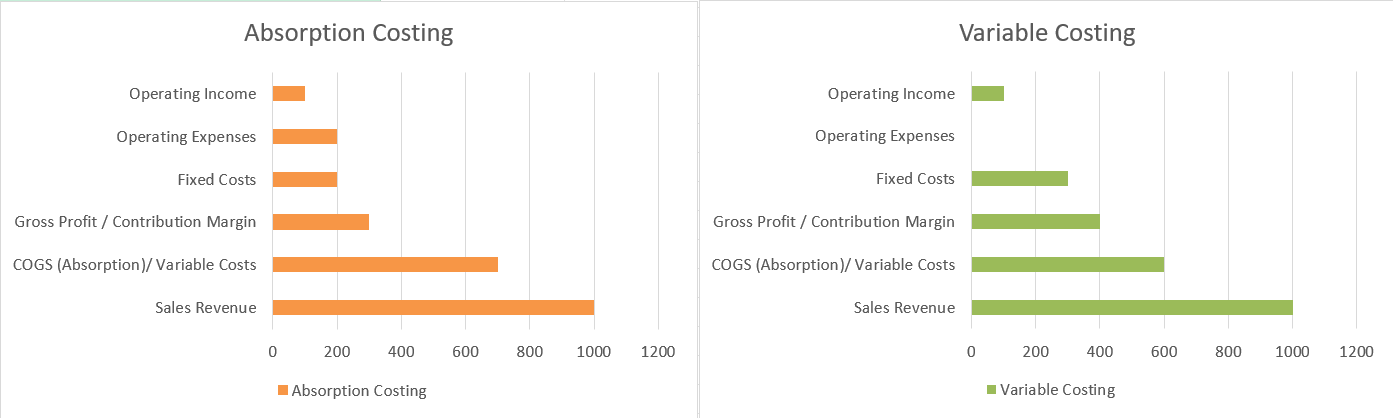

Side-by-Side Mini P&L

Use this visual when explaining the formats to non-finance stakeholders.

The Bigger Picture: From Cost to Value

Traditional costing systems—absorption, ABC, TDABC—share weaknesses like pooling and allocations that can cloud insight. Modern approaches such as Activity Value Management (AVM®) link costs to activities and stakeholder value (customer loyalty, employee engagement), with bidirectional audit trails and prescriptive analytics. Consider a dual path: adopt contribution margin for internal reporting now, while exploring value-centric frameworks for deeper performance improvement.

Conclusion: Dual Reporting for Better Decisions

- Absorption costing → external compliance and investor communication.

- Variable costing → day-to-day managerial insight via contribution margin.

Contribution margin illuminates how revenues, variable costs, and fixed expenses interact—making it a superior guide for planning, pricing, and performance management.

Next: Build your management packs around contribution margin, and add guardrails that prevent profit inflation via overproduction.

© 2025 ZubairSyed.com

zubairsyed.cma@gmail.com

M Zubair Syed is a finance leader with over 20 years of experience in FP&A and business partnering across various sectors, including automotive and e-commerce. He currently serves as Branch Accounting Manager at Al Futtaim Motors, overseeing financial management and strategic planning for multiple vehicle divisions. His achievements include AED 1.1 million in indirect cost savings and AED 45 million in working capital release. Mr. Syed is proficient in financial planning and analysis, IFRS, risk management, and digital finance tools. He holds CMA and FMVA certifications, is a CPA candidate, and has a Master's in Accounting and Finance. He has championed digital finance initiatives, enhancing reporting accuracy and operational efficiency through automation tools like SAP S/4HANA and Power BI. His previous roles include Finance Manager positions at Elabelz.com and Sap and Kaps Petroleum Services.